International. According to International Data Corporation's (IDC) Quarterly Global Cloud IT Infrastructure Tracker, vendor revenue from sales of IT infrastructure products (server, enterprise storage, and Ethernet switch) for cloud environments, including public and private cloud, increased 9.4% year-over-year in the third quarter of 2020 (3Q20). Investments in traditional IT infrastructure, not in the cloud, decreased by -8.3% year-on-year in 3Q20.

International. According to International Data Corporation's (IDC) Quarterly Global Cloud IT Infrastructure Tracker, vendor revenue from sales of IT infrastructure products (server, enterprise storage, and Ethernet switch) for cloud environments, including public and private cloud, increased 9.4% year-over-year in the third quarter of 2020 (3Q20). Investments in traditional IT infrastructure, not in the cloud, decreased by -8.3% year-on-year in 3Q20.

These growth rates show the market's response to the major adjustments in business, educational, and social activities caused by the COVID-19 pandemic and the role that IT infrastructure plays in these adjustments. Around the world, massive shifts towards online tools occurred in all aspects of human life, including collaboration, virtual business events, entertainment, shopping, telemedicine, and education. Cloud environments, and in particular the public cloud, were a key driver of this change.

Spending on IT infrastructure in the public cloud increased by 13.1% year-on-year in 3Q20, reaching US$13.3 billion. During the previous quarter, spending on it infrastructure in the public cloud outpaced spending on non-cloud IT infrastructure for the first time, but spending on non-cloud IT infrastructure returned to the top in 3Q20 with $13.7 billion.

IDC expects spending on public cloud IT infrastructure to again outpace spending on non-cloud IT infrastructure in the near future and expand its leadership. Meanwhile, private cloud infrastructure spending increased 0.6% year-over-year in 3Q20 to $5 billion, with on-premises private clouds accounting for 63.2% of this amount.

IDC believes that the hardware infrastructure market has reached a tipping point and that cloud environments will continue to account for an increasing share of total spending. With only a quarter remaining and the market stabilizing after the initial COVID-19 market shock, IDC has slightly increased its forecast for cloud IT infrastructure spending for the full year 2020, expecting growth of 11.1% to $74.1 billion. IDC lowered its forecast for non-cloud infrastructure, expecting a decrease of -11.4% to $60.2 billion. Public cloud IT infrastructure is expected to grow 16.7% year-over-year to $52.7 billion for the full year. Spending on private cloud infrastructure is expected to decline 0.5% to $21.3 billion for the full year.

As of 2019, dominance of cloud IT environments over non-cloud ones already existed for compute platforms and Ethernet switches, while most newly shipped storage platforms still resided in non-cloud environments. Starting in 2020, with the increase in investments by public cloud providers in storage platforms, this shift will continue to be persistent across all three technology domains. Within cloud deployment environments in 2020, computing platforms will continue to be the largest segment (49.1%) of spending, with growth of 2.3% to $36.4 billion, while storage platforms will be the fastest growing segment with spending increase of 27.4% to $29.2 billion, and the Ethernet switch. Segment will grow 4.0% year-over-year to $8.5 billion.

Spending on cloud IT infrastructure increased in most regions in 3Q20, with the highest annual growth rates in Canada (32.8%), China (29.4%) and Latin America (23.4%). Growth in the United States was 4.7%. Japan and Western Europe decreased by -6.7% and -3.4%, respectively. In all regions except Canada and Japan, the growth of public cloud infrastructure outpaced the growth of private cloud IT.

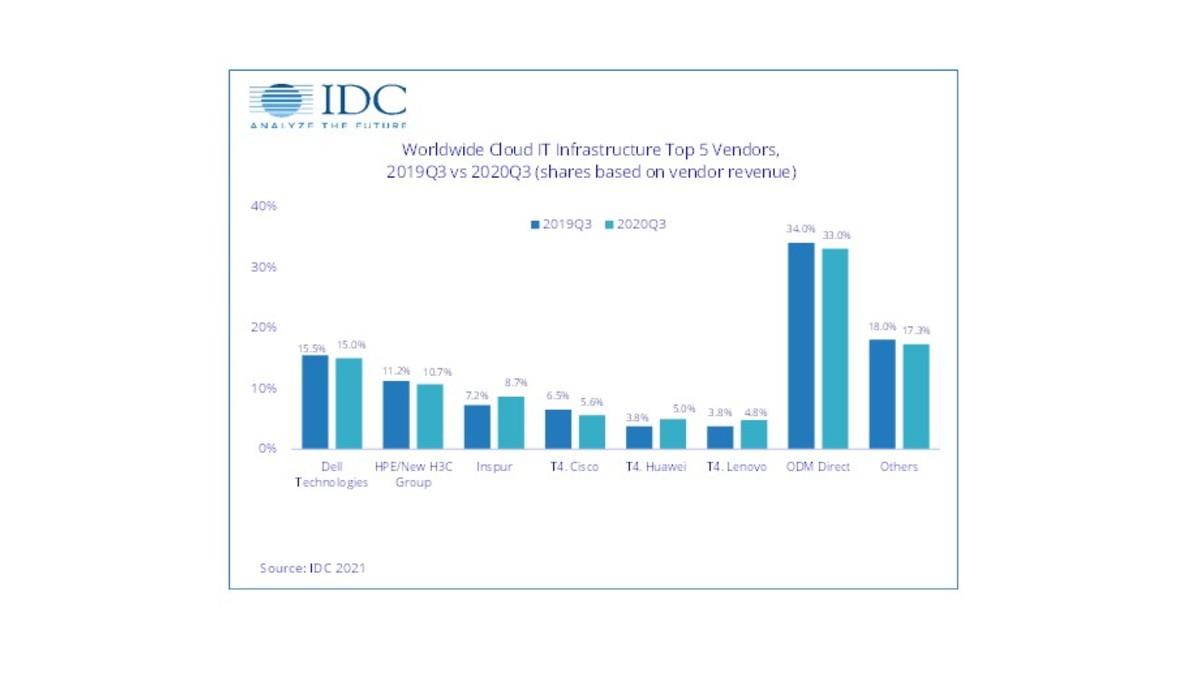

At the provider level, the results were mixed. Inspur, Huawei and Lenovo had double-digit year-over-year growth, while most other major suppliers, including the ODM Direct supplier group, had single-digit growth. Cisco was the only major vendor to post a year-over-year decline.

Top Enterprises, Revenue from Cloud IT Infrastructure Providers Worldwide, Market Share and Year-over-Year Growth, Third Quarter 2020

Notes:

* IDC declares a statistical tie in the global cloud IT infrastructure market when there is a difference of one percent or less in vendor revenue shares between two or more vendors.

a Due to the existing joint venture between HPE and the new H3C group, IDC reports the global external market share for HPE as "HPE/New H3C Group" from the second quarter of 2016 onwards.

b Due to the existing joint venture between IBM and Inspur, IDC reports the global external market share for Inspur and Inspur Power Systems as "Inspur/Inspur Power Systems" as of Q3 2018.

Source: IDC.