International. Historically, the residential alarm monitoring market has been less susceptible to economic shocks than other industries, but amid the unprecedented economic crisis caused by COVID-19, even this sector is feeling the impact.

International. Historically, the residential alarm monitoring market has been less susceptible to economic shocks than other industries, but amid the unprecedented economic crisis caused by COVID-19, even this sector is feeling the impact.

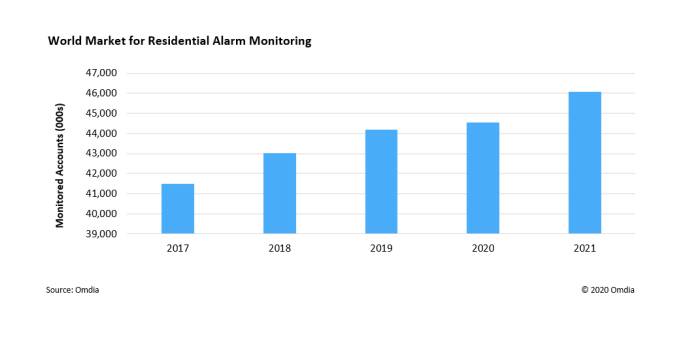

The global market for monitored residential security is expected to remain stable this year, with the number of accounts increasing by a meager 0.8 percent, according to Omdia's 2020 Residential Remote Monitoring Report. Omdia's previous forecast called for growth of 3.8 percent for the year.

"In both good economic and bad times, consumers have been willing to open their wallets to spend on residential alarm monitoring, generating steady growth in the number of accounts around the world," said Blake Kozak, principal analyst at Omdia. "However, the COVID-19 crisis is on a completely different scale than previous recessions. Not only has the pandemic affected consumer spending, but mass quarantines have flooded almost every country in the world. Consequently, the residential alarm monitoring industry is set to experience a sharp reduction in growth for the remainder of 2020."

Regional markets feel the impact

The COVID-19 pandemic is strongly impacting regional residential alarm monitoring markets. In the Europe, Middle East and Africa (EMEA) region, account growth is now expected to total 2.5 percent in 2020, more than half of the previous projection of 5.6 percent growth. The projected reduction for Asia is even more dramatic, as the number of accounts in the region is expected to rise just 1.5 percent this year, a factor of five less than the previous expectation of 7.6 percent growth.

By the end of May, there were signs that much of the United States was ready to begin a gradual approach to reopening the economy. This news is welcome for the alarm industry, especially for businesses that rely on door-to-door sales during the summer months. However, existing home sales have slowed and are expected to decline by as much as 25 percent in the United States in 2020, leading to a severe decline in new alarm account facilities.

Despite this, not everything is lost during this quiet time for new accounts, as in the United States and many other countries, installers can rely on 3G sunset (to upgrade cellular radios from 3G to 4G) to continue to enter homes and interact with customers.

Partly because of this, Omdia does not expect major cancellations of existing contracts. Instead, the slowdown will be the result of fewer new businesses.

Growth opportunities in the midst of the pandemic

Although the pandemic will affect the growth of accounts, the level of connectivity in households is at an all-time high. This presents an opportunity for residential monitored security providers to interact with customers and be able to make additional sales on connected devices, such as outdoor cameras. Such sales could help offset the slowdown in new contract growth.

Many alarm companies are now at or near their all-time highs for monthly recurring revenue (RMR). For example, Vivint now has an average monthly revenue per user (ARPU) of nearly $65. Distributors should consider this to be a positive sign for professionally installed and monitored systems, especially as Ring, Nest, and other DIY (Do-It-Yourself) systems continue to offer lower-cost monitoring.

Agile business models needed

DIY systems continue to take market share from traditional alarm providers. However, the absorption rate of these systems has not yet reached a tipping point with consumers. In fact, it is plausible that a short-term increase in DIY systems represents a net benefit for professional systems in the long run, especially since DIY system vendors frequently change their business models. As a result, the stability of these DIY brands can be unreliable, a phenomenon that can force consumers to turn to professional system providers.

This will continue to be a challenging year for residential alarm distributors, largely because these companies must send representatives to enter consumers' homes. This will require installers to put on personal protective equipment (PPE), something that could raise concerns among consumers. With safety solutions designed to promote a sense of stability and peace of mind among consumers, the emergence of workers dressed in PPE in homes could backfire.

This will continue to be a challenging year for distributors entering consumer homes, as PPE is likely to be required, in times of uncertainty, consumers are looking for security systems that provide them with peace of mind and stability. The entry of workers equipped with PPE into homes could clash with this picture.

Source: Omdia.